Five questions on energy contract negotiation

With experience on negotiating energy contracts across big parts of the world stretching from...

These are the two most frequently raised questions by energy buyers in 2025 so far as they try to understand the new energy regulatory landscape.

The first question gets a lot of coverage in news articles, the mainstream media or our own E&C blog. The second, however, doesn’t get much airtime or attention outside of the specialist energy policy press, such as Carbon Pulse (i.e., EU ETS2 could lead to higher energy bills and limited decarbonisation). This, despite the significant impact it can (and probably will) have on European households, industry and consumers in general.

In reality, this second question is often twofold:

We dive into this subject in more detail in this new blog in order to help energy professionals navigate the complexities of this new regulation.

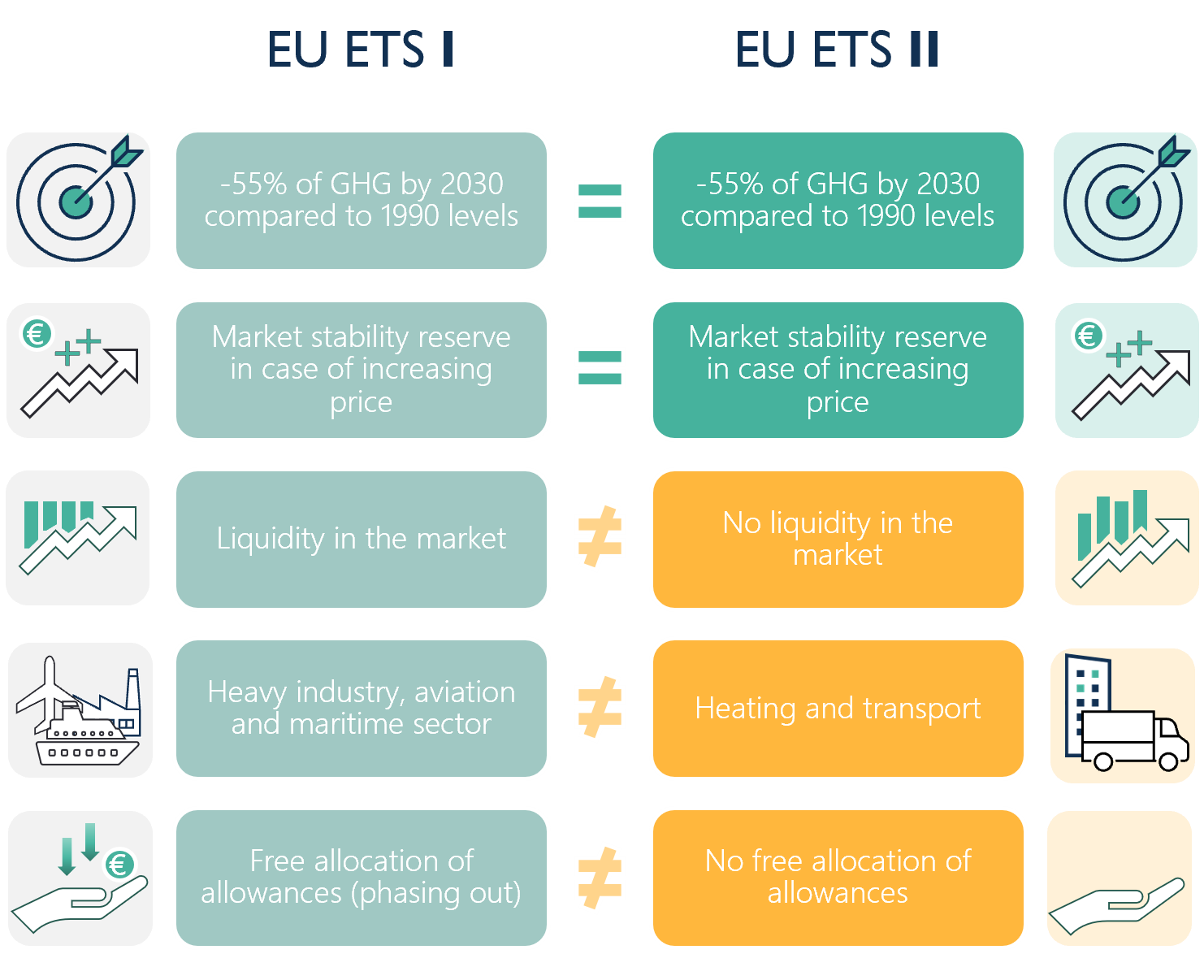

The ETS2, just like the EU ETS, is a European Trading Scheme. Based on its name, you would expect it to be very similar to its older sibling.

Yes, both are cap and trade schemes that make use of EUA auctions and a linear reduction factor (LRF) to reduce the available emissions year after year. Both also have a market stability reserve (MSR) to balance the supply and demand dynamic. But that’s more or less where the similarities stop, especially since both MSRs operate in completely different ways.

Here is a guide to the main differences between the EU ETS and ETS2:

|

EU ETS

|

|

ETS2 | |

|

Covers the heavy industry.

|

→

|

Covers the non-ETS I industry, transport and heating (the full scope of ETS II is described in Annex 3 of the EU ETS Directive).

|

|

|

Covers CO2, N²O and PFCs.

|

→

|

Only covers CO2.

The chart of the Florence School of Regulation (FSR) below provides a good overview of the relative size of EU ETS vs ETS2. It also showcases the lack of decrease of ETS2 emissions in the past 20 years and the immense challenges that lie ahead of us.

|

|

|

|||

|

Takes the emitter as the regulated entity.

|

→

|

Marks the fuel supplier as the regulated entity.

|

|

|

Has an annual deadline to hand in allowances on 30 September.

|

→

|

Has an annual deadline to hand in allowances on 31 May.

|

|

|

Mostly affects electricity prices via emissions from electricity generation.

|

→

|

Is linked to your natural gas, petrol, fuel oil, gasoline or LPG consumption: this could cover approximately 1400 regional and local gas suppliers and 3000 coal suppliers.

|

|

|

Has a long-standing history of free allocation.

|

→

|

Will not provide any free allocations, but will include intervention mechanisms. For instance, the increase of average allowance price over 45 EUR/ton for 2 subsequent months will trigger the release of 20 million allowances from the MSR.

|

|

|

When the total number of allowances in circulation exceeds 833 million, 24% of them are withdrawn from the market and stored in the MSR over a 12-month period. If it falls under 400 million, 100 million auctions are released.

|

→

|

If the total number of allowances in circulation exceeds 440 million, 100 million allowances will be moved into the MSR. If it falls under 210 million, 100 million will be released.

|

|

|

Has a functioning liquid market in place.

|

→

|

Launched on ICE on 6 May 2025 without any free allocations to provide liquidity. EEX will launch their trading as of 7 July.

|

|

While the European heavy industry has been familiar with the EU ETS for years for much smaller European industrial consumers, the launch of the ETS2 in 2027 (or 2028 in the event of “exceptionally high energy prices”) will be the start of a new reality. One where a direct cost of emission will appear, linked to gas consumption. The first impacts of this are already being felt in 2025, as most industrial consumers are contacted by their gas suppliers to provide them with input on their current gas consumption and linked emissions.

The timeline below indicates that EU member states had to implement the ETS2 into their national legislation by June 2024. Most were late with the implementation but have complied since. As the basis of the ETS II is a Directive, every member state can decide on the exact implementation itself. This means that national differences in scope, operational implementation or exemptions are bound to arise.

The FSR chart at the beginning of this article gave a good insight into the evolution of the ETS2 emissions during the past 20 years. The main question is: what lies ahead? Veyt plotted a chart (below) on the cap (and trade) development for the period 2027–2044 based on the historical Effort Sharing Regulation and the linear reduction factor (LRF) that will be used every year to bring down the cap.

The FSR chart at the beginning of this article gave a good insight into the evolution of the ETS2 emissions during the past 20 years. The main question is: what lies ahead? Veyt plotted a chart (below) on the cap (and trade) development for the period 2027–2044 based on the historical Effort Sharing Regulation and the linear reduction factor (LRF) that will be used every year to bring down the cap.

With historical ETS2 emissions of around 1200–1300 million tons, it is clear that the ETS2 cap is already below this level for 2028, which means a shortage is expected as of that moment. This shortage is partially covered by frontloading some of the allowances from the 2029–2031 cap into 2027–2028. As observed, some measures are put in place to 'soften' the early phase, but the middle- and long-term challenges will be tough.

Source: Veyt webinar, June 2024, |

Hence the second part of the questions: “What will be the impact and how do we prepare for this?”

The first impact will be an operational one. This is what we are currently noticing as the gas suppliers reach out to their clients to gather data related to their consumption and emissions in order to comply with the reporting obligations.

The second impact is felt with the appearance of ETS2 clauses in the specific and general terms and conditions when running energy supply contract tenders for the period 2027 and beyond. Most European suppliers have indeed introduced new clauses in contracts and projects, more or less detailed, on how the ETS2 cost will be passed through to the customer, as per the regulatory requirements.

Finally, the third and foremost impact will be on the price. Before the publication of ETS2 futures on any trading platforms, many speculated that the price would be situated somewhere between the 45 EUR/ton price control mechanism’s ceiling, at which more allowances would be released, and the 80 EUR/ton at which we usually see ETS I trade. Much to their surprise, the ETS2 futures trading launched on 6 May 2025, and transactions started above 73 EUR/ton with very tiny liquidity and significant bid/ask spreads.

This first publication gives some preliminary price indication, for what it’s worth at this moment in time. Energy market professionals and experts know that forecasting is near-impossible without a crystal ball, and it is no different for the price of ETS II. At this first price of 73 EUR/ton, using approximate emission factors for common fuels, this roughly translates to 15 EUR/MWh for natural gas, 25 EUR/MWh for coal and around 0,17 to 0,20 EUR/litre for fuel oil and gasoline.

During this launch period, ETS2 is trading at similar levels to EU ETS I. With no free allocation, this means the impact of the cost of emissions will be felt one-on-one in the procurement of your natural gas, fuel oil, gasoline, LPG, etc. The fuel suppliers are the regulated entities, but they will pass through the cost towards the end consumers. Therefore, it is important to start looking for ways to take control over this cost yourself via your risk management and energy contract negotiations. Those practices will take some time to settle, so it is important to start this exercise soon.

The short answer is yes. The slightly longer one is “Yes, but…”. “Yes but…” because as the start date rapidly approaches, Member States are starting to realize the impact that the implementation of the ETS2 could have on their industry and population, generating more debates and discussions around potentially revising the ETS2 before it is even operational.

Will the financial and operational impact of the ETS2 cause Member States to push for a delay of the implementation? Or will additional measures be taken under the competitiveness and simplification packages? Some suggestions to limit the impact have started to grow, but the legislative path to implement this won’t be straight forward.

From then on, there seem to be two options:

However, the European Commission closed the door to the latter option by firmly restating that “no revision of ETS2 is foreseen before 2028”.

Furthermore, last summer the European Commission launched infringement procedures against 26 Member States for incomplete transposition of climate directives for not implementing the ETS2 in national legislation in due time. This goes to show that the Commission is pushing for a timely delivery of the ETS2 and is against any type of delay, which is why it is crucial to stay up to date with regulatory evolutions.

The ETS2 system represents a significant shift in Europe's approach to carbon emissions, extending the cap-and-trade model to a wider array of sectors. As the implementation date approaches, energy buyers need to navigate the complexities of this new regulation, particularly concerning its impact on energy prices.

We invite you to register for our upcoming webinar where we will explore these changes in detail and discuss how to effectively prepare your organization for the implications of the ETS2. Don't miss this opportunity to gain expert insights and ensure you're ready for the challenges ahead.

This blog was co-written by Bart and Emma Nocquet-Wass.

Emma is an Energy Consultant specialized in Regulatory and Decarbonization and based in Paris, France.

Armed with a diverse educational background which brought her to study in France and in Germany, Emma completed her Humanities studies in Classe Préparatoire before obtaining a bachelor’s degree in political science and a master’s degree in environmental governance from Sciences Po Bordeaux. At E&C, Emma’s key areas of focus, alongside the French and Belgian markets, are the evolution of regulatory frameworks and decarbonization tools.