{kind=link}

China's dramatic energy shift has begun

It’s been a lively year in terms of power and climate policy in China as the country’s policy...

For multinational companies with significant manufacturing operations in Asia-Pacific, understanding electricity market deregulation isn't just helpful – it’s essential. This becomes even more prevalent as these companies seek to understand, track, and ultimately optimize their costs at a meter level for all sites. Being one of the only companies in the world that can accurately do this is something we are very proud of at E&C – a capability that will become particularly valuable for companies as they navigate Asia-Pacific's diverse and often opaque energy markets.

This blog series will explore the current state of electricity market deregulation in key Asian markets, beginning with China, and what it means practically for large energy buyers in terms of contracting and risk management options.

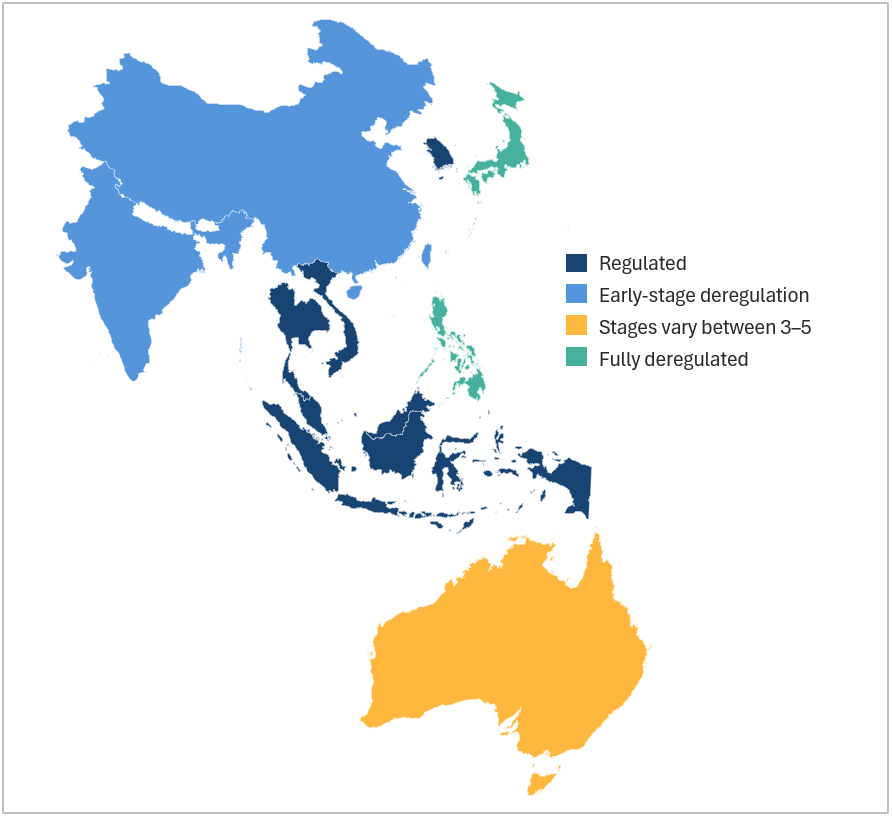

At E&C, we evaluate electricity markets using a five-category framework that helps our clients understand energy procurement and risk management possibilities in each country.

Most electricity markets in Asia Pacific currently fall between categories 1 and 2, with more advanced economies reaching categories 4 or 5. Only Australia, Japan, Singapore, and the Philippines have achieved mature stages of deregulation. Below is a snapshot of the regulatory status in countries where most of our clients have operations.

Electricity market deregulation fundamentally reshapes how power is generated, delivered, and priced, but it’s a gradual and complex process. Historically, electricity supply was controlled by state-backed monopolies to guarantee universal access. However, as economies expanded, these monopolies often became inefficient, leading to infrastructure overspending, limited innovation, and slow renewable energy integration. This inefficiency created pressure to liberalize electricity markets globally.

The move toward deregulation began in the 1980s in countries like Chile, Norway, England, and Wales. In contrast, Asia-Pacific markets started their deregulation journeys later, with Japan in the mid-1990s and China and Singapore in the early 2000s.

While deregulation has common objectives, the approach varies significantly by country. Key goals include:

Effective deregulation typically follows a structured approach: establishing independent regulation, restructuring state-owned utilities, enabling private-sector participation, and developing wholesale and retail competition. Yet, successful implementation relies heavily on regulatory independence, sufficient market liquidity, adequate infrastructure, and strong political support.

While deregulation remains a work-in-progress globally, it is particularly nuanced and complex in Asia-Pacific due to unique economic and political landscapes.

Electricity market deregulation in Asia-Pacific has taken a distinctly different path compared to Europe and North America, shaped by region-specific challenges:

As a result, reforms across the region have unfolded slowly and cautiously. Asian countries are implementing incremental market liberalization strategies – first introducing limited competition, pilot wholesale markets, and gradual price deregulation. This measured approach balances the introduction of competition with maintaining energy security, reliability, and affordability.

Though progress is uneven, steady advancements in renewable energy integration, cross-border energy trade, and market transparency continue. For multinational companies managing energy procurement across multiple Asian markets, this gradual but significant shift requires navigating diverse regulatory landscapes and adapting procurement strategies to local market realities.

China is the world’s largest electricity producer, generating about 30% of global electricity – primarily from domestic coal resources, supplemented by renewables and hydropower. By the end of 2024, China reached around 520 GW of wind and over 880 GW of solar capacity, making it the global leader in renewable energy deployment (RMI). The rapid growth of its electricity sector, which expanded sixfold from 2000 to 2021, reflects China's remarkable economic rise, but this growth has also significantly impacted the climate. Today, China contributes around 30% of global CO₂ emissions, placing the transformation of its electricity system at the centre of worldwide climate action efforts. China's ambitious goals, peaking carbon emissions by 2030 and achieving carbon neutrality by 2060, require a fundamental shift in how the country produces, distributes, and consumes power.

Source: RMI

|

While China boasts abundant energy resources, a significant geographic imbalance exists between production and consumption. Northern and western regions are rich in coal, wind, and hydro resources, whereas industrial demand is concentrated in eastern and southern provinces. This mismatch results in price disparities and ongoing challenges in balancing electricity supply and demand across the country.

To address these challenges, China has made substantial investments in Ultra-High Voltage (UHV) transmission networks, aiming to facilitate efficient electricity transfer between resource-rich inland provinces and coastal demand centres. However, grid construction and upgrades have struggled to keep pace with the rapid expansion of renewable energy projects. For instance, it takes roughly three years to approve and build new UHV transmission lines, while large-scale renewable projects can be operational in just one or two years. This timing mismatch means renewable energy often remains stranded, unable to reach high-demand markets efficiently, resulting in curtailment. Market mechanisms have yet to provide sufficient incentives for grid companies to proactively expand transmission capacity, highlighting the need for better-coordinated planning and investment decisions.

|

|

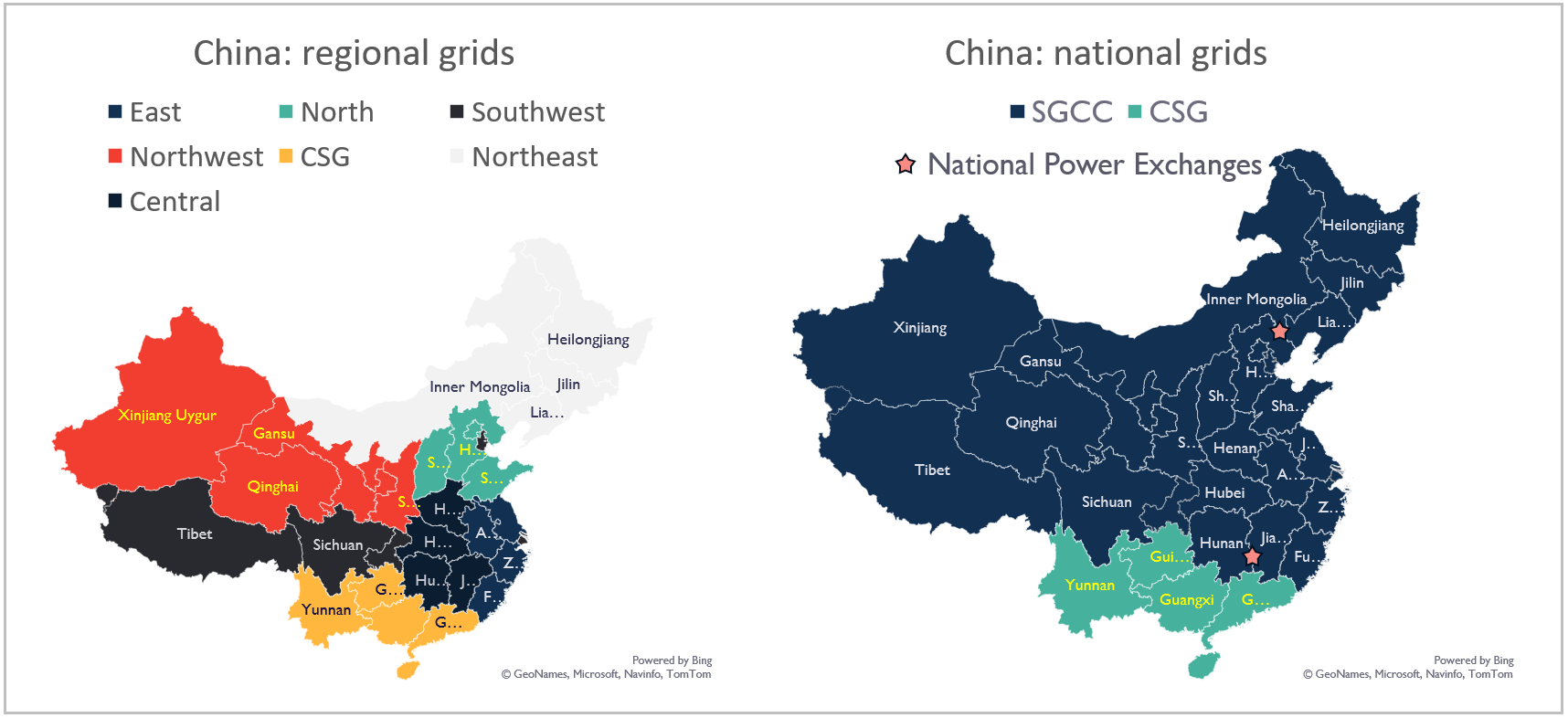

Although market reforms have accelerated in recent years, China's electricity market remains regionally fragmented. Each province manages its own power supply and dispatch priorities under the broader structure of two national grids: the State Grid (covering most of China) and China Southern Power Grid. The State Grid itself is further divided into six regional grids, adding layers of complexity.

Electricity market trading volumes have increased significantly in recent years, from roughly 1,632 TWh in 2017 to 5,254 TWh in 2022, representing over 60% of China's total electricity consumption. However, most trading remains within individual provinces (more than 80%), underscoring the persistence of provincial fragmentation. Additionally, in 2022, 79% of electricity was traded on the medium-to-long-term market, highlighting the strength of multi-day, weekly, monthly, quarterly, or annual electricity wholesale trading versus the provincial spot markets. These spot markets, which started trial operations in 2018, are part of the broader strategy to establish a unified power market. Their structure resembles that of Northern Europe, a zonal system defined at a provincial level rather than the US variant of nodal spot pricing (one price per node connected to the grid).

Nonetheless, despite infrastructure improvements and a national strategic priority given to establishing a national electricity market via an expansion of the spot markets and intra-province trading, outdated dispatch rules and limited cross-provincial grid capacity continue to restrict effective inter-provincial electricity exchange. As of 2022, intra-province trading only represented 1% of total traded electricity in China.

Source: International Monetary Fund

|

These limitations have particularly hindered renewable energy integration. Provinces with abundant wind and solar resources experience significant energy curtailment, as the grid lacks the flexibility to manage variable renewable supply effectively. Meanwhile, high-demand coastal regions continue relying heavily on local coal generation and imported LNG, highlighting the urgent need for further reforms in market mechanisms, grid flexibility, and regional coordination to fully capitalize on China's renewable energy potential.

Addressing these issues is vital, not only for China's energy transition and climate commitments, but also for large energy consumers navigating the complex electricity procurement landscape in the country.

China’s electricity sector historically operated under centralized state control, where fixed government-set tariffs ensured stability but limited competition and market responsiveness. Rapid economic expansion and rising fuel costs exposed significant inefficiencies in this system, prompting market-oriented reforms starting in 2015. Document No. 9 marked the initial step toward liberalization, requiring the separation of generation from grid management, introducing provincial power exchanges, and moving gradually away from fixed government tariffs, especially for industrial consumers.

Between 2016 and 2020, reforms expanded further, allowing large energy users to directly negotiate medium-to-long-term contracts with generators rather than relying solely on regulated tariffs. In late 2021, the market took another significant step by permitting coal-fired generation prices to fluctuate within a ±20% range around benchmark levels, introducing meaningful flexibility for generators. Around the same time, the government launched pilot wholesale electricity markets in several provinces, marking a shift from centrally planned dispatch toward market-based electricity trading. Then, in 2024, China introduced a two-part pricing mechanism for coal plants, combining capacity payments to maintain a reliable supply with market-based energy pricing responsive to real-time fuel costs.

However, progress remained uneven. Many provinces were slow to adopt competitive pricing, and state-owned grid operators retained significant influence over how power was dispatched. Additionally, regional market fragmentation persisted, making it difficult to transfer electricity efficiently across provincial borders.

Finally, in 2025, renewable generators received equal recognition. The Renewable Energy Price Settlement Mechanism was launched in 2025, fully integrating renewables into competitive markets and moving away from subsidy-dependent Feed-in Tariffs (FITs).

Recognizing these challenges, China took a major step forward in 2024 with the release of the National Unified Power Market Development Plan, also known as Document No. 118. Unlike earlier reforms, which focused on provincial and regional market pilots, this plan formalizes the timeline for a fully integrated national electricity market by 2030. Its key objectives include:

Now, as China progresses toward a unified national power market by 2029, its key challenge will be overcoming regional imbalances and creating a truly competitive and transparent electricity system. The success of this transformation will depend on how effectively China navigates the complex interplay between regional markets, renewable integration, and market-driven price signals.

Despite significant market reforms, China’s electricity sector remains heavily influenced by state-owned entities. The State Grid Corporation manages about 80% of China’s transmission and distribution infrastructure, with China Southern Power Grid controlling the southern regions. Generation is dominated by five major state-owned enterprises, the 'Big Five' (China Huaneng, China Datang, China Huadian, SPIC, and China Energy Investment Corp), which limits broader market competition.

While independent power producers (IPPs), especially renewable-focused firms, are gradually entering wholesale markets, retail competition remains constrained. Most electricity supply to end-users continues to flow through subsidiaries of these major state-owned generators, restricting the competitive choices available to many consumers.

For large industrial users, deregulation has introduced valuable but incremental benefits.

Companies now have greater flexibility, including the ability to negotiate directly with generators or participate in provincial electricity exchanges and source suppliers, moving away from rigid, state-set tariffs. Although the new market-based contracts offer enhanced negotiation power, they remain relatively short-term (typically one month to one year), with pricing strongly tied to generation costs influenced by fuel prices and supplier margins. The recent decrease in coal prices has helped drive electricity cost reductions in recent years.

Deregulation has broadened the range of available contract structures, allowing large consumers to better manage their exposure to market volatility. Current procurement options include fixed-price contracts for cost certainty, blended contracts combining fixed and monthly market prices, and shared-risk contracts that distribute market fluctuations between suppliers and users.

Green energy procurement has also become more accessible, driven by multinational companies' growing sustainability commitments. Businesses can now secure renewable electricity through short-term agreements using Green Energy Certificates (GECs), though these arrangements often lack the long-term price stability many global buyers seek.

Long-term renewable Power Purchase Agreements (PPAs) are in early stages but gaining interest. Short-term renewable PPAs (1–3 years) are increasingly common, allowing businesses to achieve sustainability targets and benefit from cheaper GECs. However, longer-term PPAs with guaranteed additionality, highly desirable for global corporations, are still rare and generally restricted to the largest foundational energy consumers. Regulatory uncertainty and grid integration challenges currently limit broader adoption, although growth in this area is expected.

As China moves towards a unified national power market by 2029, overcoming regional imbalances and establishing a genuinely competitive and transparent market will be critical. For large energy buyers, navigating this evolving landscape presents both significant opportunities and ongoing complexities, underscoring the need for an informed energy procurement strategy.

Looking ahead, China’s electricity market reforms will deepen further, emphasizing expanded real-time spot market trading, enhanced retail competition, and greater integration across provincial borders. The National Unified Power Market Development Plan (Document No. 118, 2024) clearly outlines these priorities, aiming for a fully integrated national market by 2030.

Successfully implementing these reforms will require overcoming persistent regional disparities, updating dispatch rules, and improving transmission infrastructure to effectively support renewable energy integration.

For large industrial and commercial energy buyers, these ongoing changes present significant opportunities to optimize costs, manage procurement risks, and achieve sustainability goals.

Yet, successfully navigating China's evolving electricity market will continue to demand a strategic approach given the existing complexities, limited retail supplier diversity, and ongoing regulatory evolution.

Companies operating in China must remain agile and informed to fully capitalize on the benefits of market liberalization. Are you prepared for Asia-Pacific's changing energy landscape?